Across the United States, more than fifty million retired men and women are currently drawing monthly Social Security checks, a financial lifeline that has become a defining feature of retirement life in America. Yet, although these benefits are established by federal policy, the exact amount a retiree pockets each month can differ substantially depending on where they have chosen to spend their later years. Geographic location, cost-of-living differences, and local economies often influence how generous or modest one’s monthly payment appears when compared to others across state lines.

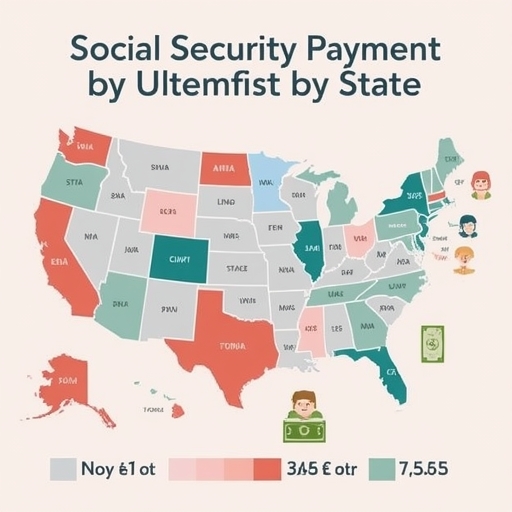

For example, retirees living along the East Coast tend to receive noticeably higher median monthly payments than those residing in a number of Southern states. This is partly reflective of regional income levels during individuals’ working years, which directly affect Social Security benefit calculations. However, while East Coast recipients may enjoy larger nominal checks, they frequently encounter higher state taxes or cost-of-living adjustments that can reduce the effective value of their income. Data compiled for the Social Security Administration’s 2025 *Annual Statistical Supplement* highlights that New Jersey and Connecticut stand out as the states where retired workers are most likely to collect the highest benefit amounts.

In New Jersey specifically, retirees have a median monthly benefit of approximately $2,172—the most substantial figure recorded nationwide. This stands in sharp contrast to Louisiana and Mississippi, where the median monthly payments hover closer to $1,726, representing the lower end of the national spectrum. According to figures from the Social Security Administration as of November 2025, the nationwide average monthly payout to retired workers was roughly $1,960. That number is poised to rise modestly in the upcoming year, thanks to a 2.8% cost-of-living adjustment designed to help beneficiaries keep pace with ongoing inflation. For states such as New Jersey and Connecticut, where payments already exceed the national average, this increase could translate into even greater monthly earnings, further widening the disparity between regions.

Nonetheless, the size of one’s Social Security check only tells part of the larger story surrounding financial security in retirement. For millions of older adults, these payments represent the principal, and sometimes the sole, source of monthly income. Others find themselves compelled to remain in the workforce—whether part-time or through freelance work—well beyond the traditional retirement age simply to make ends meet. Persistent inflation and the continuing rise in the cost of essential goods and services—such as groceries, utilities, and medical care—have further strained retirees’ budgets, eroding the purchasing power of their benefits and limiting how far each check can stretch.

A separate analysis by AARP, drawing on data from the University of Massachusetts Boston’s *Elder Index*, offers deeper insight into the real-world adequacy of Social Security income. The Elder Index measures the minimum amount older adults need to live independently with basic security, accounting for variable factors such as housing costs, healthcare expenses, food, transportation, and regional price differences. According to AARP’s findings, Social Security benefits alone fail to fully cover the cost of these essentials in every state across the country. Still, the degree of shortfall varies: benefits provide relatively better coverage in more affordable regions such as Indiana, West Virginia, and Alabama, where lower living costs allow payments to stretch further.

The contrast is particularly striking in a high-cost-of-living state like New Jersey. While retirees there receive a median of about $2,190 per month, AARP’s analysis estimated that an older homeowner who still carries a mortgage faces average monthly expenses of $4,149—nearly double the median Social Security benefit. This gap illustrates the enduring financial tension experienced by many retirees who must reconcile fixed incomes with ever-increasing costs of daily life. Ultimately, these statistics underscore both the indispensable role of Social Security in sustaining aging Americans and the limitations that compel many to supplement their benefits through savings, investments, or continued employment.

If you personally rely on Social Security or find yourself struggling to manage living costs while receiving your monthly benefits, the reporter welcomes your experiences and insights. You can reach out directly at jkaplan@businessinsider.com to share how the program impacts your daily financial reality.

Sourse: https://www.businessinsider.com/map-social-security-payments-by-state-2025-12